Updated in June 2026

Crypto Institutional Adoption: How Wall Street, ETFs, Stablecoins and Tokenization Are Reshaping Digital Assets

Crypto institutional adoption is no longer a distant narrative. It is already changing the structure of the digital asset market. Bitcoin ETFs, regulated custody, tokenized funds, stablecoin payment rails, real-world asset tokenization and bank-led blockchain initiatives are gradually turning crypto from a speculative parallel market into a new layer of financial infrastructure.

The most important point is simple: institutional adoption does not mean that crypto has become less volatile. Bitcoin can still fall sharply, ETF flows can reverse, and altcoins can collapse during risk-off periods. But the market is no longer driven only by retail speculation, memes or halving narratives. It is increasingly influenced by asset managers, banks, corporate treasuries, payment companies, regulators and large investors looking for compliant exposure to digital assets.

In this updated analysis, we look at the latest trends behind crypto institutional adoption, the rise of Bitcoin ETFs, the growing role of stablecoins, the acceleration of tokenized real-world assets, the impact of AI and blockchain convergence, and the scenarios that could shape the market through 2026 and 2027.

Key Takeaways: Crypto Institutional Adoption in 2026

- Bitcoin ETFs have changed market access: institutions can now gain exposure without directly managing private keys, wallets or on-chain custody.

- BlackRock, Fidelity and other major asset managers have made crypto exposure easier to integrate into traditional portfolios.

- Stablecoins are becoming financial infrastructure: they are increasingly used for settlement, cross-border payments, DeFi liquidity and dollar access.

- Tokenized real-world assets are accelerating: US Treasuries, money market funds, private credit and commodities are moving on-chain.

- Banks are no longer ignoring blockchain: tokenized deposits, custody, settlement systems and digital asset trading are becoming strategic priorities.

- The next phase is not only Bitcoin: crypto institutional adoption is moving toward stablecoins, tokenization, Web3 infrastructure and AI-driven financial systems.

Crypto Institutional Adoption Has Entered a New Phase

For years, the crypto market waited for “institutions” as if adoption would arrive in one dramatic moment. In reality, crypto institutional adoption has been a gradual process. First came trading desks. Then came custody platforms. Then regulated futures. Then corporate treasury experiments. Then spot Bitcoin ETFs. Now the market is moving toward tokenized funds, stablecoins, bank-grade infrastructure and 24/7 settlement.

This is a major shift. Early crypto was built around the idea of escaping traditional finance. The new phase is different. Traditional finance is not disappearing. It is absorbing parts of crypto infrastructure and adapting them to its own needs.

That does not mean the original crypto thesis is dead. Bitcoin remains a scarce, decentralized monetary asset. Ethereum and other smart contract networks still support permissionless applications. DeFi still offers alternatives to banks and brokers. But the direction of travel is clear: institutions want regulated access, controlled risk, audited infrastructure and products that can be integrated into existing portfolios.

Why institutions are adopting crypto now

Several forces explain why crypto institutional adoption has accelerated:

- Regulated investment vehicles: spot Bitcoin ETFs and crypto-linked funds reduce operational friction for traditional investors.

- Custody maturity: institutional custody has become more professional, insured, audited and integrated with trading platforms.

- Client demand: wealth managers, family offices and hedge funds increasingly face demand for crypto exposure.

- Macroeconomic uncertainty: debt, inflation risk and currency debasement narratives continue to support long-term interest in Bitcoin.

- Stablecoin growth: dollar-backed tokens have become one of the clearest real-world use cases of blockchain technology.

- Tokenization: asset managers see blockchain as a way to improve settlement, transparency and distribution.

Important nuance

Crypto institutional adoption does not remove risk. It changes the type of risk. Instead of a purely retail-driven market, crypto is increasingly exposed to ETF flows, macro data, liquidity conditions, regulatory decisions, custody risk, compliance requirements and institutional rebalancing.

Bitcoin ETFs: The Most Visible Sign of Crypto Institutional Adoption

The launch and growth of spot Bitcoin ETFs remain the clearest symbol of crypto institutional adoption. Before these products, many institutions had to choose between direct Bitcoin custody, futures-based exposure, private funds or no exposure at all. Spot ETFs changed that equation.

For traditional investors, ETFs offer a familiar wrapper. They can be bought through brokerage accounts, integrated into model portfolios, analyzed through traditional fund metrics and held without managing seed phrases or private keys. This does not make Bitcoin less volatile, but it makes access easier.

BlackRock’s iShares Bitcoin Trust, Fidelity’s Wise Origin Bitcoin Fund and other products have created a new gateway between traditional capital markets and Bitcoin. The scale matters because institutional investors often move slowly. They allocate through committees, risk models, compliance processes and custody policies. ETFs fit that structure far better than direct wallet-based ownership.

What Bitcoin ETFs changed

- Accessibility: Bitcoin became easier to buy for advisors, funds and traditional investors.

- Legitimacy: the presence of major asset managers reduced the reputational barrier around Bitcoin.

- Liquidity: ETF trading added another layer of market depth.

- Portfolio integration: Bitcoin can now be included in traditional allocation models.

- Risk management: exposure can be monitored, rebalanced and reported through standard fund infrastructure.

However, ETF adoption also creates a more two-sided market. When inflows are strong, ETFs can amplify structural demand. When investors reduce risk, ETF outflows can add pressure. This is why crypto institutional adoption should not be confused with permanent price support. Institutions can buy, but they can also sell.

Market Reality: ETFs Are Powerful, But Not Magic

Bitcoin ETFs make institutional adoption easier, but they do not eliminate volatility. In a risk-off environment, ETF holders can reduce exposure just like they would with technology stocks, gold ETFs or high-yield bonds. The difference is that Bitcoin is now more deeply connected to global liquidity and traditional market sentiment.

From Bitcoin Exposure to Digital Asset Infrastructure

The first stage of crypto institutional adoption was about access to Bitcoin. The second stage is about infrastructure. Institutions are no longer asking only: “Should we hold Bitcoin?” They are asking broader questions:

- Can stablecoins improve payment settlement?

- Can tokenized money market funds reduce operational friction?

- Can blockchain rails support 24/7 capital markets?

- Can tokenized deposits compete with private stablecoins?

- Can real-world assets become more liquid through on-chain representation?

- Can AI agents interact safely with smart contracts and digital wallets?

This is where the story becomes much larger than Bitcoin. Crypto is evolving from an asset class into a financial technology stack.

Stablecoins: The Institutional Use Case That Already Works

Stablecoins are one of the strongest examples of real-world blockchain usage. While Bitcoin is often viewed as digital gold and Ethereum as a smart contract platform, stablecoins are already used as digital dollars for trading, settlement, remittances, DeFi liquidity and cross-border transfers.

For institutions, stablecoins are attractive because they solve a practical problem: moving value quickly across digital networks. Traditional banking settlement can be slow, limited by business hours and dependent on intermediaries. Stablecoins can operate 24/7, settle rapidly and interact with programmable financial applications.

Why stablecoins matter for crypto institutional adoption

- Payments: stablecoins can reduce friction in cross-border transfers.

- Settlement: they allow near-instant movement of dollar-like value between platforms.

- DeFi liquidity: stablecoins are the base layer of many lending, trading and yield markets.

- Emerging markets: they provide digital dollar access where local currencies are unstable.

- Tokenization: stablecoins can serve as the cash leg for tokenized assets.

This is why stablecoins may become even more important than many speculative tokens. They are not designed to rise 10x. Their value lies in utility, liquidity and integration. In that sense, stablecoins are not just a crypto product. They are part of the payment and settlement infrastructure that could support the next stage of crypto institutional adoption.

Stablecoin Trend to Watch

The key question for 2026 and 2027 is not whether stablecoins will exist. They already do. The real question is who will dominate the market: crypto-native issuers, regulated fintech companies, banks, payment networks, or tokenized deposit systems built by traditional financial institutions.

Tokenized Real-World Assets: The Bridge Between Crypto and Traditional Finance

Real-world asset tokenization is another major driver of crypto institutional adoption. The idea is simple: represent off-chain assets on-chain. These assets may include US Treasuries, money market funds, private credit, real estate, commodities, equities or bonds.

In practice, tokenization is complex. A token is not automatically the asset itself. It may represent a claim, a share, a beneficial interest or a contractual right. Legal structure, custody, redemption rules, compliance, liquidity and jurisdiction matter enormously. But despite these challenges, tokenization is gaining momentum because institutions see clear operational benefits.

Why institutions care about tokenization

- Faster settlement: blockchain networks can reduce delays in clearing and settlement.

- 24/7 markets: tokenized assets can theoretically trade outside traditional market hours.

- Programmable compliance: transfer restrictions can be embedded into token logic.

- Operational transparency: ownership and transfer history can be tracked on-chain.

- New distribution channels: asset managers can reach digitally native investors.

Tokenized Treasuries and money market funds are especially important because they combine a familiar asset class with blockchain settlement. BlackRock’s BUIDL fund is often cited as a major example of institutional tokenization, while platforms such as Securitize, Ondo Finance, Franklin Templeton and others show how traditional financial products can move closer to on-chain infrastructure.

The Tokenization Warning

Tokenization does not automatically create liquidity. A tokenized asset can still be illiquid, restricted to approved investors, dependent on off-chain legal agreements and concentrated among a small number of holders. The future winners will not simply be the projects that tokenize assets, but those that create trusted, liquid and compliant markets around them.

Banks Are Building Their Own Blockchain Strategy

One of the biggest changes in crypto institutional adoption is the attitude of banks. Years ago, many banks dismissed crypto as a threat or a speculative bubble. Today, the largest financial institutions are exploring digital asset custody, tokenized deposits, blockchain settlement, stablecoin strategies and crypto trading infrastructure.

This does not mean banks are becoming fully decentralized. In many cases, they are adopting blockchain technology without adopting crypto’s original permissionless philosophy. Their goal is not necessarily to replace the financial system, but to make it faster, more programmable and more competitive against crypto-native companies.

Bank-led crypto adoption may include:

- Tokenized deposits: bank deposits represented on blockchain rails.

- Institutional custody: secure storage solutions for digital assets.

- Settlement networks: faster transfers between financial institutions.

- Trading services: crypto execution for hedge funds and large clients.

- Tokenized collateral: using digital assets or tokenized securities in institutional finance.

This trend is crucial. If banks build tokenized deposit systems, they may compete directly with stablecoins. If asset managers tokenize funds, they may compete with DeFi yield products. If exchanges offer tokenized equities, they may compete with traditional brokerages. The result is not a simple victory for crypto or banks. It is a convergence.

Web3 Infrastructure: The Rails Behind Institutional Adoption

While Bitcoin ETFs and stablecoins get most of the attention, Web3 infrastructure is the foundation that makes deeper adoption possible. Without scalable networks, secure custody, reliable oracles, bridges, data availability layers and compliance tools, crypto institutional adoption cannot reach its full potential.

Institutions require infrastructure that is resilient, auditable and scalable. They cannot rely only on narratives. They need uptime, liquidity, reporting, regulatory compatibility and counterparty risk controls.

Key infrastructure categories to watch

- Layer 2 networks: Arbitrum, Optimism, Base and other scaling solutions reduce costs and improve throughput.

- Data availability: modular infrastructure helps blockchains scale without sacrificing verification.

- Oracles: Chainlink and other oracle systems connect smart contracts to real-world data.

- Custody platforms: institutional custody is essential for asset managers, banks and corporations.

- Compliance tools: AML, analytics, whitelisting and reporting systems make regulated adoption possible.

- Interoperability: institutions need secure movement of assets across multiple chains and platforms.

In this sense, Web3 infrastructure may be one of the strongest long-term beneficiaries of crypto institutional adoption. The market may speculate on tokens, but the real economic value often flows to the rails that institutions actually use.

AI and Blockchain: The Next Institutional Frontier

AI is becoming a major theme in digital assets. The connection between AI and blockchain is still early, but the potential is significant. AI can analyze data, make decisions and automate workflows. Blockchain can provide ownership, settlement, identity, payments and auditability.

Together, they could support autonomous financial agents, AI-managed portfolios, decentralized compute markets, smart contract security tools and machine-to-machine payments. This may sound futuristic, but the institutional logic is clear: if AI systems are going to act economically, they need payment rails, identity frameworks, audit trails and programmable contracts.

Potential use cases of AI blockchain convergence

- Autonomous agents: AI systems that execute transactions, manage wallets or interact with DeFi protocols.

- Smart contract auditing: AI tools that detect vulnerabilities before deployment.

- On-chain risk monitoring: real-time detection of liquidity, leverage and counterparty risk.

- Decentralized compute: blockchain-based networks for GPU access and AI workloads.

- Automated treasury management: AI systems optimizing stablecoin, tokenized Treasury and crypto positions.

AI + Crypto: Opportunity and Risk

AI blockchain convergence could become a major growth theme, but investors should remain careful. Many projects will use AI as a marketing label. The strongest opportunities will likely be found in infrastructure: oracles, compute, security, data, identity, payments and agent-compatible smart contract systems.

How Crypto Institutional Adoption Changes Market Cycles

Previous crypto cycles were easier to explain. Bitcoin halving, retail speculation, liquidity expansion, altcoin season, then collapse. This pattern still matters, but it is no longer enough. Crypto institutional adoption has added new drivers.

Today, crypto reacts to:

- ETF inflows and outflows

- Federal Reserve rate expectations

- US dollar liquidity

- technology stock performance

- regulatory votes and enforcement actions

- stablecoin supply growth

- corporate treasury decisions

- risk appetite across global markets

This makes crypto more mature, but also more connected to traditional markets. Bitcoin can still behave like a scarce monetary asset over the long term, but in the short term it often trades like a high-volatility risk asset. That is one of the paradoxes of institutional adoption: it gives crypto more legitimacy, but also exposes it to the same macro forces that move stocks, bonds and commodities.

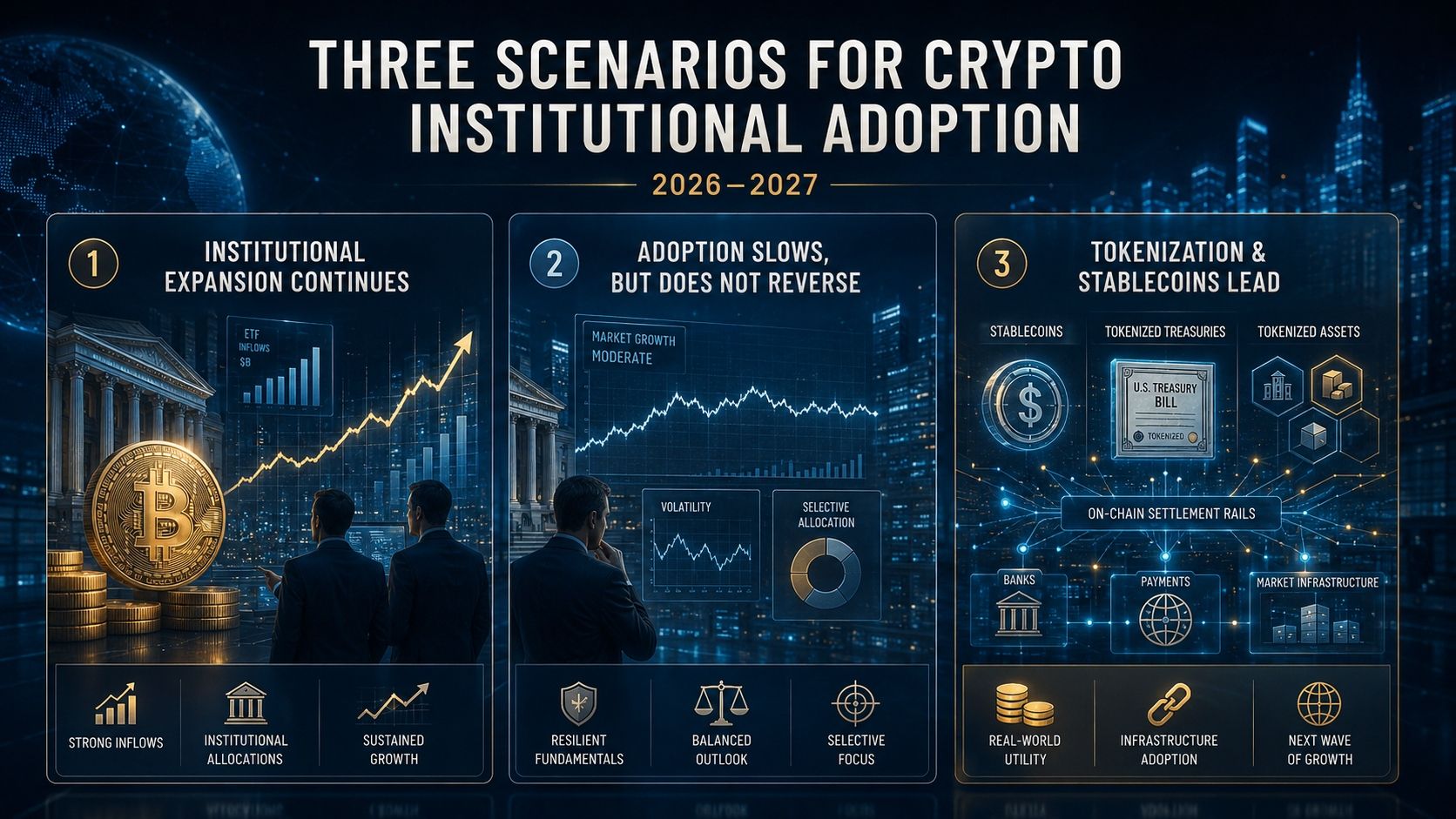

Three Scenarios for Crypto Institutional Adoption in 2026–2027

Scenario 1: The Institutional Expansion Continues

Probability: Moderate to high

In this scenario, crypto institutional adoption continues despite volatility. Bitcoin ETFs remain a core access point, Ethereum and other major networks gain more institutional attention, stablecoins become increasingly integrated into payment systems, and tokenized funds keep growing.

What would support this scenario?

- renewed ETF inflows after periods of market stress

- clearer regulation around stablecoins and market structure

- more banks offering crypto custody or trading services

- larger tokenized Treasury and money market fund adoption

- greater use of stablecoins in payments and settlement

Likely winners: Bitcoin, Ethereum, stablecoin infrastructure, tokenization platforms, custody providers, compliant DeFi protocols and institutional-grade Web3 infrastructure.

Scenario 2: Institutional Adoption Slows, But Does Not Reverse

Probability: Moderate

In this scenario, weak prices, ETF outflows, regulatory delays or macro pressure slow the pace of adoption. Institutions do not abandon crypto, but they become more selective. Bitcoin remains the preferred institutional asset, while smaller altcoins struggle to attract serious capital.

What would support this scenario?

- continued high interest rates or tighter liquidity

- weak ETF demand for several months

- major hacks or custody failures

- regulatory uncertainty around DeFi or tokenized securities

- poor performance of speculative crypto products

Likely winners: Bitcoin, regulated stablecoins, top custody platforms, security providers and projects with real revenue or institutional usage.

Scenario 3: Tokenization and Stablecoins Become the Main Story

Probability: Increasing into 2027

In this scenario, the center of gravity shifts away from pure crypto price speculation and toward financial infrastructure. Stablecoins, tokenized deposits, tokenized Treasuries, money market funds and on-chain settlement become the main drivers of adoption.

What would support this scenario?

- banks launching tokenized deposit networks

- payment companies integrating stablecoins

- asset managers expanding tokenized fund offerings

- regulators providing clearer rules for digital cash and tokenized securities

- corporates using blockchain rails for treasury and settlement

Likely winners: stablecoin issuers, tokenization platforms, regulated DeFi infrastructure, payment networks, oracle providers and compliance-focused blockchain rails.

The Big Trend Ahead

The next phase of crypto institutional adoption will probably be less about “which token can go up the fastest” and more about “which infrastructure can handle real financial activity.” Bitcoin remains central, but stablecoins, tokenized assets, custody, compliance, settlement and AI-compatible infrastructure may define the next institutional cycle.

What Investors Should Watch Now

For investors, the most important mistake would be to reduce crypto institutional adoption to a simple bullish slogan. Adoption is real, but it is uneven. It benefits some assets and weakens others. It rewards liquidity, security, compliance and utility. It punishes fragile tokenomics, weak governance and projects with no real demand.

Key metrics to monitor

- Bitcoin ETF flows: inflows show institutional demand; outflows reveal risk-off pressure.

- Stablecoin supply: growth often signals more liquidity entering the crypto ecosystem.

- Tokenized RWA value: especially Treasuries, money market funds and private credit.

- DeFi revenue: real fees matter more than inflated TVL.

- Custody growth: institutions need secure storage before allocating serious capital.

- Regulation: stablecoin laws, market structure bills and securities rules can accelerate or slow adoption.

- Bank activity: tokenized deposits, settlement pilots and custody launches show where finance is heading.

Portfolio Implications of Crypto Institutional Adoption

A reasonable framework for understanding the market is to separate crypto assets into four categories:

1. Monetary assets

Bitcoin remains the leading institutional monetary asset in crypto. It benefits from scarcity, liquidity, brand recognition, ETF access and a simple narrative. For many institutions, Bitcoin is still the first and sometimes only crypto allocation.

2. Infrastructure assets

Ethereum, Layer 2 networks, oracles, interoperability protocols and data availability solutions support the applications institutions may eventually use. These assets are more complex than Bitcoin, but they may capture value if on-chain activity grows.

3. Financial utility assets

Stablecoins, tokenized Treasuries, DeFi lending protocols and tokenization platforms are closer to financial infrastructure. Their value depends less on ideology and more on usage, liquidity, compliance and trust.

4. Speculative innovation assets

AI crypto projects, autonomous agent platforms, decentralized compute networks and early-stage Web3 systems may offer high upside but also high risk. Many will fail. A few could become important if AI and blockchain converge at scale.

Investor Framework

In a more institutional market, the strongest crypto assets are likely to combine at least one of these qualities: liquidity, regulatory compatibility, security, real usage, strong network effects, revenue generation or deep integration with financial infrastructure.

Risks: What Could Slow Crypto Institutional Adoption?

Even if the long-term trend is positive, several risks could slow crypto institutional adoption.

- Regulatory fragmentation: conflicting rules between the US, Europe and Asia could limit global adoption.

- Custody failures: a major institutional custody incident would damage trust.

- Stablecoin stress: redemption pressure or reserve concerns could affect market confidence.

- Tokenization disappointment: if tokenized assets remain illiquid, the market may question the use case.

- Macro pressure: high rates and tighter liquidity can reduce demand for risk assets.

- DeFi exploits: smart contract vulnerabilities remain a major barrier for institutions.

- Over-financialization: too many products with weak demand could lead to closures and investor fatigue.

These risks do not invalidate the trend. They show why institutional adoption will likely be selective. The market may become more professional, but also more ruthless.

Conclusion: Crypto Institutional Adoption Is Reshaping the Market, But Not in the Way Many Expected

Crypto institutional adoption is real, but it is not a simple story of Wall Street buying every token. It is a structural transformation of access, custody, settlement, payments, tokenization and financial infrastructure.

Bitcoin ETFs brought the first major wave of traditional capital into crypto. Stablecoins are proving that blockchain can move money globally. Tokenized real-world assets are showing how traditional finance can move on-chain. Banks are building their own blockchain strategies. AI may create a new generation of autonomous financial systems. And Web3 infrastructure is becoming the invisible layer behind all of it.

The market will remain volatile. ETF flows will rise and fall. Bitcoin can still experience deep corrections. Many altcoins will fail. But the deeper trend is difficult to ignore: crypto is no longer only a retail rebellion. It is becoming part of the financial system it once tried to replace.

The key question for the next cycle is therefore not only whether Bitcoin will rise. The real question is: who will control the infrastructure of digital finance?

Will it be banks with tokenized deposits? Asset managers with tokenized funds? Stablecoin issuers? Public blockchains? DeFi protocols? AI agents? Or a hybrid system where all of them compete on the same rails?

That is the real story behind crypto institutional adoption. It is not just about price. It is about the future architecture of money, markets and digital value.

Read More on Digital Assets

To follow the latest market developments, institutional trends, Bitcoin analysis and DeFi updates, visit our main DeFi News page.

Disclaimer: This article on crypto institutional adoption is for informational and educational purposes only. It does not constitute financial advice, investment advice or a recommendation to buy or sell any cryptocurrency, token, ETF or financial product. Digital assets remain volatile and risky. Always do your own research and consult a qualified financial professional before making investment decisions.