Robinhood Chain is no longer just a roadmap or an experimental test network. Robinhood officially launched the blockchain’s mainnet on July 1, 2026, marking a major step in the company’s attempt to connect traditional investing, tokenized stocks, real-world assets and decentralized finance.

The project matters because Robinhood is not a small crypto startup trying to attract its first users. It is one of America’s best-known retail brokerage platforms, with an established customer base across stocks, exchange-traded funds, options, retirement products and cryptocurrencies.

When a brokerage of this scale launches its own blockchain, the message is difficult to ignore: tokenization is moving beyond crypto-native experiments and becoming part of the strategic plans of major financial platforms.

Robinhood wants its network to support tokenized stocks and ETFs, decentralized exchanges, borrowing and lending, real-world assets, perpetual markets and increasingly automated financial services.

Yet there is a striking contradiction at the center of the project. Robinhood is an American company building infrastructure around tokenized American securities, but its Stock Tokens are not currently available to investors in the United States.

That makes the most important question larger than “What is Robinhood Chain?”

The real question is:

Can Robinhood use blockchain technology to create a new global distribution layer for U.S. financial markets—and will American investors eventually be allowed to participate?

What Is Robinhood Chain?

Robinhood Chain is a public blockchain developed by Robinhood for tokenized assets and onchain financial applications. Its mainnet officially went live on July 1, 2026, following the launch of a public testnet in February.

The network was built using the Arbitrum technology stack and remains connected to the broader Ethereum ecosystem. It is therefore not an entirely independent Layer 1 blockchain comparable to Bitcoin, Solana or Avalanche.

Instead, Robinhood Chain is a dedicated Ethereum-compatible network designed to give Robinhood greater control over transaction execution, fees, integrations and the user experience surrounding its financial products.

This distinction is important.

Robinhood did not create a general-purpose blockchain simply to compete for crypto activity. The network has a more focused objective: becoming an infrastructure layer for tokenized financial markets.

Its intended uses include:

- Tokenized public stocks and ETFs

- Real-world assets, commonly known as RWAs

- Decentralized exchanges and token swaps

- Onchain lending and borrowing

- Collateralized financial products

- Perpetual and derivatives markets

- Automated and AI-assisted investing tools

- Applications created by outside developers

The blockchain is also public, which matters because Robinhood is not positioning it merely as an internal settlement database. The company wants wallets, protocols, developers and liquidity providers to connect to the network and build services around its tokenized assets.

Robinhood Chain Mainnet Is Now Live

The original Robinhood blockchain announcement dates back to June 2025, when the company introduced Stock Tokens for eligible European customers and revealed plans to develop a dedicated Layer 2 network.

At first, those assets were issued and processed through Arbitrum One while Robinhood prepared its own infrastructure.

A public testnet followed in February 2026, allowing developers to experiment with test assets, wallet integrations and Ethereum-compatible applications.

The project entered a new phase on July 1, 2026, when Robinhood announced that the Robinhood Chain mainnet was live.

This transition is significant. A testnet is designed primarily for development and experimentation. A mainnet is a functioning production network capable of supporting real assets, applications and economic activity.

Robinhood’s strategy illustrates what Arbitrum describes as a “launch-and-migrate” model. A company can initially launch products on an established network such as Arbitrum One, test demand and user behavior, and later move activity onto a dedicated blockchain offering more customization.

For Robinhood, greater control could eventually make it easier to:

- Subsidize or simplify transaction fees

- Integrate identity and compliance systems

- Manage the lifecycle of tokenized securities

- Coordinate liquidity across Robinhood products

- Design a smoother experience for non-crypto users

- Support specific institutional or regulatory requirements

The launch does not mean that every planned feature is immediately mature or widely adopted. It does mean, however, that Robinhood Chain has moved beyond being a theoretical future product.

Key takeaway: Robinhood Chain is now a live, public blockchain designed to connect tokenized stocks, real-world assets, DeFi services and Robinhood’s global distribution network.

Robinhood Chain Records Explosive Early Trading Activity

Only days after its mainnet launch, Robinhood Chain recorded one of the strongest starts seen among recent blockchain networks. Its decentralized exchanges briefly processed more daily spot volume than Hyperliquid, while stablecoin liquidity, lending deposits and the number of available trading pairs increased rapidly.

The surge was supported by major DeFi integrations such as Uniswap and Morpho, but also by speculative activity involving newly launched tokens and memecoins. This distinction matters: the early numbers show that Robinhood Chain can attract traders and liquidity, but they do not yet prove that the network has achieved sustainable adoption.

For a detailed analysis of the volumes, leading tokens and the reasons behind this sudden growth, read our latest report: Robinhood Chain Volume Surges Past Hyperliquid: What Is Driving It?

Why Is Robinhood Building Its Own Blockchain?

Robinhood could have continued using Ethereum, Arbitrum One or another existing network. Launching a dedicated chain requires technical resources, security planning, developer support and ongoing ecosystem development.

The decision therefore reflects a broader strategic ambition.

More control over the user experience

Most Robinhood customers are not blockchain specialists. They may understand stocks, ETFs and crypto prices without understanding gas fees, token bridges, seed phrases or smart-contract approvals.

For Robinhood Chain to reach a mass audience, much of this complexity must disappear into the background.

Controlling the network gives Robinhood more freedom to design an experience in which blockchain infrastructure functions almost invisibly. Users could eventually interact with tokenized assets without having to manage every technical detail normally associated with decentralized finance.

A unified financial ecosystem

Robinhood already operates across several areas of retail finance. A dedicated blockchain could help connect services that currently exist in separate technological environments.

Stocks, ETFs, cryptocurrencies, stablecoins, tokenized assets, lending products and derivatives could gradually become part of one programmable financial system.

The result would not necessarily look like a traditional crypto wallet. It could look like a familiar brokerage application whose settlement, collateral and asset-transfer functions increasingly operate onchain.

Ownership of the financial rails

Brokerages traditionally depend on exchanges, clearing firms, custodians, market makers, banks and payment networks. Blockchain technology does not eliminate all of these intermediaries, particularly when regulated securities are involved.

However, it may allow Robinhood to control a larger portion of the infrastructure connecting users to financial assets.

That control can be strategically valuable. It can reduce dependence on outside systems, create new sources of revenue and make it easier to launch proprietary products.

A global distribution opportunity

Robinhood’s Stock Tokens are particularly relevant outside the United States.

Demand for U.S. equities is global, but direct access to American markets can remain costly or complicated in some countries. Tokenized products give Robinhood another way to distribute economic exposure to U.S. companies internationally.

Robinhood Chain could therefore become a global financial rail for American assets, even before those same tokenized products become available to American retail investors.

Stock Tokens Are at the Center of Robinhood’s Strategy

The most important assets on Robinhood Chain are Stock Tokens: blockchain-based instruments tied to the economic performance of stocks or ETFs.

Depending on the product and jurisdiction, eligible users may gain exposure to companies such as Nvidia, Apple or Alphabet, as well as major exchange-traded funds.

These products are designed to combine familiar market exposure with features associated with crypto infrastructure, including:

- Fractional access to expensive securities

- Extended or potentially continuous trading hours

- Blockchain-based settlement

- Programmable ownership and transfer rules

- Integration with wallets and DeFi applications

- Possible use as collateral

This could eventually change how investors interact with stocks.

Instead of remaining locked inside a conventional brokerage account, a tokenized financial asset might be transferred to a wallet, exchanged through a decentralized protocol or deposited into a lending application.

But an important warning is necessary: a Stock Token is not automatically the same thing as directly owning a share.

Is a Robinhood Stock Token the Same as a Real Share?

No—not necessarily.

Robinhood has explained that some of its Stock Tokens are tokenized contracts designed to track the value of underlying securities. The precise legal structure and investor rights can vary according to the type of token and the jurisdiction in which it is offered.

An investor should not assume that purchasing a token tied to Nvidia, Apple or another company automatically creates direct ownership of a registered corporate share.

Potential differences can include:

- No direct registration as a shareholder

- No voting rights

- Different dividend mechanisms

- Claims against the token issuer rather than the underlying company

- Dependence on a broker, custodian or special-purpose vehicle

- Different legal protections in the event of insolvency

- Restrictions on transfers or redemptions

The structure becomes even more complicated when a token provides exposure to a privately held company rather than a publicly traded stock.

Robinhood previously attracted attention by introducing products linked to private companies such as OpenAI and SpaceX. OpenAI publicly clarified that Robinhood’s token did not represent direct OpenAI equity and had not been issued in partnership with the company.

That episode demonstrates why investors must distinguish between three different ideas:

- Owning an actual share

- Owning a token backed by or linked to a share

- Owning a contractual product that merely follows the share’s value

These products may provide similar economic exposure under normal market conditions, but their legal and counterparty risks are not identical.

Why Robinhood Stock Tokens Are Not Available in the United States

One of the most important facts for an American audience is that Robinhood’s Stock Tokens are currently unavailable in the United States.

This may seem surprising. Robinhood is headquartered in the U.S., the underlying companies are often American, and the blockchain itself is presented on Robinhood’s American website.

The reason is primarily regulatory.

Offering a blockchain-based representation of a security to American retail investors raises questions involving securities registration, custody, broker-dealer rules, market structure, clearing, investor disclosures and secondary trading.

A tokenized stock is not simply another cryptocurrency. If it represents or tracks a security, it enters one of the most heavily regulated areas of the American financial system.

Robinhood has therefore launched these products first in eligible international markets, where the company can operate under different regulatory frameworks.

This does not mean American access will remain impossible forever.

In June 2026, Reuters reported that the U.S. Securities and Exchange Commission was preparing a potential framework that could allow crypto companies to test tokenized-stock trading through a limited “innovation exemption.”

Such an exemption could give platforms including Robinhood and Coinbase a path toward offering tokenized securities under controlled conditions before a broader regulatory framework is finalized.

However, the proposal remains controversial.

Supporters argue that tokenization could modernize American capital markets by enabling faster settlement, longer trading hours, greater competition and programmable financial products.

Critics—including some traditional market firms and industry associations—warn that experimental exemptions could weaken investor protections or create fragmented liquidity outside established exchanges.

Robinhood Chain is therefore not only a technology project. It is also part of a broader debate over how U.S. stock markets should evolve.

Could Tokenized Stocks Come to U.S. Investors?

The possibility is becoming more credible, but it is not guaranteed.

The SEC’s evolving approach suggests that regulators are taking tokenized securities seriously. Major exchanges and financial firms are also exploring blockchain-based trading and settlement.

Several conditions would likely need to be addressed before Robinhood Stock Tokens become widely available to American retail investors:

- Clear rules defining the legal status of the tokens

- Investor disclosures explaining ownership and counterparty risks

- Approved custody arrangements

- Reliable market surveillance

- Mechanisms preventing price manipulation

- Standards for reserves and underlying asset backing

- Rules governing transfers between wallets and platforms

- Coordination with existing securities exchanges and clearing systems

A limited pilot program appears more plausible than an immediate nationwide rollout without restrictions.

For Robinhood, regulatory approval in the United States would be strategically important. The company already has the customers, brand recognition and brokerage infrastructure needed to introduce tokenized investing to a mainstream audience.

Until that approval arrives, however, American readers should view Robinhood Chain as a network created by a U.S. company whose most distinctive investment products are primarily directed toward international users.

Why Arbitrum Was Chosen for Robinhood Chain

Robinhood Chain uses the Arbitrum technology stack, which is designed to support Ethereum-compatible networks with lower transaction costs and greater throughput.

This choice offers several advantages.

Ethereum compatibility

Developers familiar with Ethereum can use many of the same programming tools and smart-contract standards on Robinhood Chain.

That reduces the difficulty of building wallets, exchanges, lending protocols and tokenization applications for the network.

Access to an established ecosystem

Ethereum remains one of the most important ecosystems for stablecoins, decentralized finance and tokenized real-world assets.

Building with Arbitrum allows Robinhood Chain to remain connected to this environment rather than starting from an isolated Layer 1 network with no developers or liquidity.

Customization

A dedicated Arbitrum-based chain can be configured around Robinhood’s needs.

This may include specialized fee policies, transaction sequencing, governance controls, compliance integrations and tools designed for regulated financial products.

A gradual migration strategy

Robinhood was able to launch its initial Stock Tokens on Arbitrum One before moving toward its own blockchain.

This reduced the risk of developing an entire network before confirming demand for the underlying products.

Robinhood Chain therefore demonstrates how major financial companies may adopt blockchain infrastructure without launching a completely independent cryptocurrency network from the beginning.

Robinhood Chain and DeFi

The most ambitious part of the project is not merely the issuance of tokenized stocks. It is the potential integration of those assets into decentralized finance.

In a conventional brokerage account, a stock can generally be bought, held, sold or sometimes lent. Its use is constrained by the systems and services offered by the brokerage.

An onchain asset can theoretically become more composable.

A Stock Token could be:

- Swapped through a decentralized exchange

- Deposited into a lending protocol

- Used as collateral for borrowing

- Combined with stablecoins in a liquidity pool

- Included in an automated investment strategy

- Used within a structured financial product

This is where Robinhood Chain could become far more important than a simple token-issuance system.

If tokenized stocks can circulate through multiple applications, Robinhood would be helping create a programmable market in which traditional securities interact with crypto-native infrastructure.

Early integrations with decentralized trading and wallet providers suggest that Robinhood wants outside applications to connect with the network.

However, the same composability that creates innovation can also increase risk.

If a tokenized stock is widely used as collateral, a failure involving its issuer, pricing oracle, liquidity provider or underlying custodian could affect several connected protocols.

DeFi has repeatedly shown that interconnected systems can transmit stress quickly. Adding securities and other regulated assets may make these relationships even more complex.

Can Robinhood Chain Offer 24/7 Stock Trading?

The promise of continuous markets is one of tokenization’s strongest selling points.

Cryptocurrencies can be traded around the clock, while U.S. stock exchanges still operate around defined sessions. Brokerages have expanded premarket, after-hours and overnight trading, but the underlying market structure is not fully continuous.

Tokenized stocks could potentially trade 24 hours a day, seven days a week.

But trading a token around the clock does not mean that the underlying stock market is also open.

When Nasdaq or the New York Stock Exchange is closed, a token linked to a listed stock may face:

- Wider bid-ask spreads

- Lower liquidity

- Greater divergence from the underlying share price

- Uncertainty during major weekend news

- More difficult hedging for market makers

For example, a token linked to a technology company might trade sharply lower on a Sunday after unexpected news. The official stock would not begin regular trading until Monday.

Market makers would need to estimate where the stock might reopen, creating additional volatility and pricing risk.

Continuous access can be useful, but it does not automatically guarantee continuous liquidity or accurate pricing.

Why Tokenized Stocks Attract So Much Interest

Tokenized stocks appeal to fintech companies, crypto platforms and global investors for several reasons.

Global access to U.S. markets

American companies represent a large share of global equity-market value. Investors around the world want exposure to technology, artificial intelligence, semiconductors, healthcare and consumer brands listed in the United States.

Tokenization can create new distribution channels in countries where opening and funding a traditional U.S. brokerage account may be difficult.

Fractional investing

A token can be divided into very small units. This makes high-priced assets more accessible to investors with limited capital.

Fractional investing already exists through conventional brokerages, but blockchain infrastructure can make those fractions more portable and programmable.

Faster settlement

Traditional securities transactions rely on clearing and settlement systems that have improved considerably but still involve multiple institutions.

Blockchain transactions can potentially settle much faster, although legal ownership and offchain custody may still require additional processes.

Programmability

A tokenized asset can interact with software.

Smart contracts could automate collateral management, dividend distribution, portfolio rebalancing, lending or structured-product payouts.

This programmability is one of the clearest differences between simply displaying a stock balance in an app and representing financial exposure on a blockchain.

Integration with stablecoins

Stablecoins could become the cash layer of tokenized financial markets.

An investor might move from a dollar-backed stablecoin into a tokenized ETF, use the ETF token as collateral and later return to stablecoins without relying on a traditional bank transfer at every stage.

Robinhood Chain appears designed around this broader vision of interoperable financial assets.

Robinhood Chain and the Growth of Real-World Assets

Robinhood’s project is part of the expanding real-world asset sector.

RWAs are traditional or offchain assets represented through blockchain-based tokens. The category can include:

- U.S. Treasury bills

- Money-market funds

- Corporate and government bonds

- Private credit

- Commodities

- Real estate

- Stocks and ETFs

Stablecoins provided the first large-scale demonstration that an offchain asset—the U.S. dollar—could be represented and transferred effectively on public blockchains.

Tokenized Treasury products then showed that investors could access yield-bearing traditional assets through onchain systems.

Stocks and ETFs represent the next major frontier because they are widely understood, globally demanded and deeply connected to the existing financial system.

Robinhood Chain could accelerate this trend by combining tokenized assets with a recognizable consumer brand and an existing financial application.

How Robinhood Chain Compares With Base, Ethereum, Solana and Avalanche

Robinhood Chain is sometimes presented as a potential competitor to other major blockchain networks. The comparison is useful, but it requires nuance.

Ethereum

Ethereum remains the dominant settlement and smart-contract ecosystem for many stablecoins, DeFi protocols and tokenized assets.

Robinhood Chain does not attempt to replace Ethereum entirely. Its use of the Arbitrum stack keeps it closely connected to the Ethereum environment.

Base

Base is especially relevant because it is backed by Coinbase, another major American crypto and financial platform.

Both Coinbase and Robinhood have large customer-distribution channels and want to move more financial activity onchain.

Base has developed as a broad consumer and application ecosystem. Robinhood Chain appears more narrowly focused on tokenized securities, real-world assets and financial services linked to Robinhood.

Solana

Solana offers high throughput, low transaction fees and a fast consumer experience. Its ecosystem has attracted decentralized exchanges, stablecoin payments, tokenized assets and retail trading applications.

Robinhood Chain’s main advantage over Solana is not necessarily raw technical performance. It is Robinhood’s direct integration with brokerage products and customers.

To understand the broader role of Solana in onchain finance, discover the Solana ecosystem and its main applications.

Avalanche

Avalanche has pursued institutional tokenization and customizable blockchain infrastructure for several years.

Its strategy of creating purpose-built networks has similarities with Robinhood’s decision to launch a dedicated chain.

The distribution advantage

Robinhood Chain’s strongest competitive advantage is distribution.

Blockchain technology alone rarely guarantees adoption. A network also needs users, liquidity, applications and recognizable products.

Robinhood already has a widely used app, a large customer base and a strong position in retail investing. The company’s challenge is converting that distribution into genuine onchain activity.

Could Robinhood Chain Become a Walled Garden?

Robinhood describes the network as a public blockchain, and outside wallets and applications can connect to it.

Nevertheless, a central strategic question remains: how open will the ecosystem become in practice?

A technically public blockchain can still depend heavily on one company for:

- Asset issuance

- Customer access

- Compliance approval

- Liquidity

- Transaction ordering

- Key infrastructure services

Robinhood may prefer a controlled environment because regulated assets require identity checks, jurisdictional restrictions and investor-protection measures.

Developers, however, may hesitate to build major applications if one company can substantially change access or product conditions.

The future of Robinhood Chain may therefore depend on its ability to balance two conflicting goals:

the openness expected from public blockchains and the control required for regulated financial products.

Does Robinhood Chain Have Its Own Token?

Robinhood has not positioned a new speculative network token as the central feature of Robinhood Chain.

This is an important distinction from many earlier blockchain launches, which relied on a native token to fund development, reward validators, attract liquidity or generate market attention.

The absence of a heavily promoted token allows Robinhood to focus the narrative on products and infrastructure rather than speculation.

Users should be cautious of unofficial assets attempting to use the Robinhood Chain name. A token bearing a similar name is not automatically issued, supported or endorsed by Robinhood.

The network’s future fee and governance structure may evolve, but investors should rely only on Robinhood’s official communications when assessing any asset claiming a connection to the blockchain.

The Role of AI and Agentic Finance

Robinhood’s July 2026 announcement extended beyond blockchain and tokenized stocks. The company also emphasized agentic and AI-supported financial products.

The concept of agentic finance refers to software agents capable of analyzing information and performing certain financial tasks with a degree of automation.

In an onchain environment, AI agents could theoretically:

- Monitor collateral positions

- Rebalance portfolios

- Find liquidity across decentralized exchanges

- Compare lending rates

- Execute predefined risk-management strategies

- Identify unusual market conditions

Blockchain infrastructure can make these systems easier to automate because assets and transactions follow programmable standards.

However, agentic finance introduces additional risks. An automated system can execute mistakes at high speed, react to inaccurate data or follow an objective that does not fully reflect the user’s interests.

The combination of tokenized securities, DeFi and AI could become one of Robinhood Chain’s most innovative features—but also one of its most sensitive.

Major Robinhood Chain Risks

Robinhood Chain has considerable potential, but investors and developers should understand the risks.

1. Confusing a token with direct stock ownership

This remains the most immediate investor risk.

A token tracking a stock’s price may not provide direct ownership, voting rights or the same legal protections as a conventional share.

2. Regulatory risk

Rules governing tokenized securities differ between countries and may change rapidly.

A product available in one jurisdiction may be restricted, modified or removed in another. The United States remains particularly important because Robinhood’s Stock Tokens are not currently available there.

3. Counterparty risk

Tokenized assets may depend on an issuer, custodian, broker, special-purpose vehicle or reserve manager.

Investors are exposed not only to the market value of the underlying asset but also to the entities maintaining the token’s legal and financial structure.

4. Liquidity risk

A token can reference one of the world’s most liquid stocks while remaining relatively illiquid itself.

Token liquidity depends on market makers, exchanges, wallet support, jurisdictional restrictions and real user demand.

5. Smart-contract risk

Applications running on Robinhood Chain may contain programming errors or security vulnerabilities.

A problem involving a decentralized exchange, lending protocol, bridge or token contract could cause financial losses.

6. Oracle risk

Tokenized assets need reliable external price data.

If an oracle reports an incorrect price, a lending protocol might liquidate users unfairly or allow undercollateralized borrowing.

7. Bridge and interoperability risk

Assets moving between Robinhood Chain, Ethereum, Arbitrum or other networks may rely on bridges.

Bridges have historically been among the most frequently attacked components of the crypto ecosystem.

8. Centralization risk

Although Robinhood Chain is public, Robinhood may retain substantial influence over its infrastructure, asset issuance and access policies.

This may be necessary for regulatory compliance but can limit the decentralization users normally associate with public blockchains.

9. Market-hours mismatch

Tokenized assets may trade when the underlying stock exchange is closed.

This can create price gaps, weaker liquidity and higher volatility outside regular market hours.

Important: Robinhood Chain may simplify access to onchain finance, but it does not eliminate financial risk. It changes where that risk is located—from traditional brokers and clearing systems toward token issuers, custodians, smart contracts, oracles and blockchain infrastructure.

Why Robinhood Chain Matters to Wall Street

Robinhood Chain matters beyond the crypto market because it challenges assumptions about how securities must be issued, traded and settled.

The American equity market is one of the deepest and most efficient financial systems in the world. It also relies on a complex network of exchanges, broker-dealers, clearing firms, transfer agents, custodians and regulators.

Tokenization proposes a different architecture:

- Assets represented through programmable tokens

- Near-continuous trading

- Faster settlement

- Direct integration with digital wallets

- Automated collateral and compliance rules

Traditional market firms are unlikely to disappear. Many of them may instead adopt similar technology.

Nasdaq, the New York Stock Exchange, major banks and asset managers are already examining blockchain-based settlement or tokenized financial products.

Robinhood’s advantage is its willingness to build directly for retail users and move more quickly than many established institutions.

Its disadvantage is that regulated markets require trust, stability and investor protection at a scale that crypto infrastructure has not always demonstrated.

Robinhood Chain: Revolution or Gradual Evolution?

It would be an exaggeration to claim that Robinhood Chain will immediately replace conventional stock markets.

The New York Stock Exchange, Nasdaq, clearing agencies, regulated custodians and major brokerages will not become obsolete simply because tokenized assets can circulate on a public blockchain.

It would also be a mistake to dismiss the project as a marketing exercise.

Robinhood Chain is live. Robinhood has already launched tokenized-market products internationally. Wallets and DeFi applications are beginning to integrate with the network. U.S. regulators are actively debating pathways for tokenized stock trading.

The most realistic conclusion lies between the extremes.

Robinhood Chain may not transform global finance overnight, but it could accelerate a gradual migration of financial assets toward programmable infrastructure.

The project will be judged by several measurable factors:

- Real trading activity

- Liquidity outside Robinhood’s own application

- Developer adoption

- Security and network reliability

- Clarity around token-holder rights

- Regulatory approval in major markets

- Eventual access for American users

Conclusion: Robinhood Chain Opens a New Chapter for Tokenized Finance

Robinhood Chain represents one of the clearest attempts by a mainstream American brokerage to build financial products directly on blockchain infrastructure.

The network combines several of the crypto market’s most important trends: Ethereum scaling, tokenized stocks, real-world assets, decentralized finance, stablecoin settlement and automated investing.

Its greatest strength is Robinhood’s ability to distribute products to a large audience. Many blockchain projects have strong technology but struggle to attract users. Robinhood begins with an established brand, financial licenses, a widely used application and experience serving retail investors.

Its greatest challenge is regulation.

The project’s central paradox remains striking: Robinhood has created a blockchain designed in large part around American financial assets, but American customers cannot currently access its Stock Tokens.

That could change as the SEC develops its approach to tokenized securities. If a workable regulatory framework emerges, Robinhood would be well positioned to become one of the first platforms to offer blockchain-based stock products to a mass U.S. audience.

Until then, Robinhood Chain is best viewed as both a functioning blockchain and a large-scale experiment.

It is testing whether stocks, ETFs and other regulated assets can become portable, programmable and compatible with decentralized financial applications—without sacrificing the investor protections expected from traditional markets.

If the experiment succeeds, blockchain will no longer operate only as an alternative financial system.

It could become part of the infrastructure supporting mainstream global markets.

Robinhood Chain FAQ

What is Robinhood Chain?

Robinhood Chain is a public, Ethereum-compatible blockchain developed by Robinhood for tokenized stocks, ETFs, real-world assets and onchain financial applications. It was built using the Arbitrum technology stack.

Is Robinhood Chain live?

Yes. Robinhood officially launched the Robinhood Chain mainnet on July 1, 2026, after operating a public testnet earlier in the year.

Is Robinhood Chain a Layer 2 blockchain?

Robinhood describes the network as an Ethereum-compatible chain built with Arbitrum technology. It is designed to benefit from the Ethereum and Arbitrum development ecosystem while giving Robinhood more control over its own financial infrastructure.

What are Robinhood Stock Tokens?

Robinhood Stock Tokens are blockchain-based products tied to the economic performance of stocks or ETFs. Their exact structure and investor rights depend on the specific product and jurisdiction.

Are Stock Tokens the same as owning real shares?

Not necessarily. A Stock Token may track a stock’s value without providing direct shareholder registration, voting rights or the same legal protections as owning a conventional share.

Can U.S. investors buy Robinhood Stock Tokens?

No. Robinhood states that its Stock Tokens are not currently available in the United States. Availability also remains subject to restrictions in other jurisdictions.

Why are Robinhood Stock Tokens unavailable in the U.S.?

Tokenized securities raise complex questions involving SEC registration, custody, broker-dealer regulation, market surveillance and investor protection. A clearer regulatory pathway is needed before widespread U.S. distribution becomes possible.

Could Robinhood Stock Tokens become available in America?

Possibly. The SEC has been considering potential frameworks and limited exemptions for tokenized securities. However, the timing, conditions and final regulatory requirements remain uncertain.

Does Robinhood Chain have a native token?

Robinhood has not made a speculative native token the central feature of the network. Users should be cautious of unofficial tokens claiming an association with Robinhood Chain.

What can developers build on Robinhood Chain?

Developers may build wallets, decentralized exchanges, lending platforms, trading tools, real-world asset applications and other Ethereum-compatible financial services, subject to the network’s rules and applicable regulations.

Can Robinhood Stock Tokens be traded 24/7?

Blockchain infrastructure can support continuous trading, but individual products may have specific schedules. Liquidity and pricing can also be less reliable when the underlying U.S. stock market is closed.

How is Robinhood Chain connected to Arbitrum?

Robinhood Chain was built using the Arbitrum technology stack. Robinhood initially launched Stock Tokens on Arbitrum One before moving toward a dedicated blockchain environment.

Can Robinhood Chain compete with Base or Solana?

Robinhood Chain may compete for financial applications and tokenized assets, but its positioning is more specialized. Its main advantage is Robinhood’s brokerage infrastructure and existing global distribution.

What are the main Robinhood Chain risks?

The main risks include regulatory uncertainty, confusion between tokens and direct stock ownership, counterparty exposure, limited liquidity, smart-contract vulnerabilities, oracle failures, bridge attacks and potential centralization.

Why is Robinhood Chain important in 2026?

Robinhood Chain is important because it is one of the largest tests of whether a mainstream brokerage can connect stocks, ETFs, real-world assets and decentralized finance through a public blockchain.

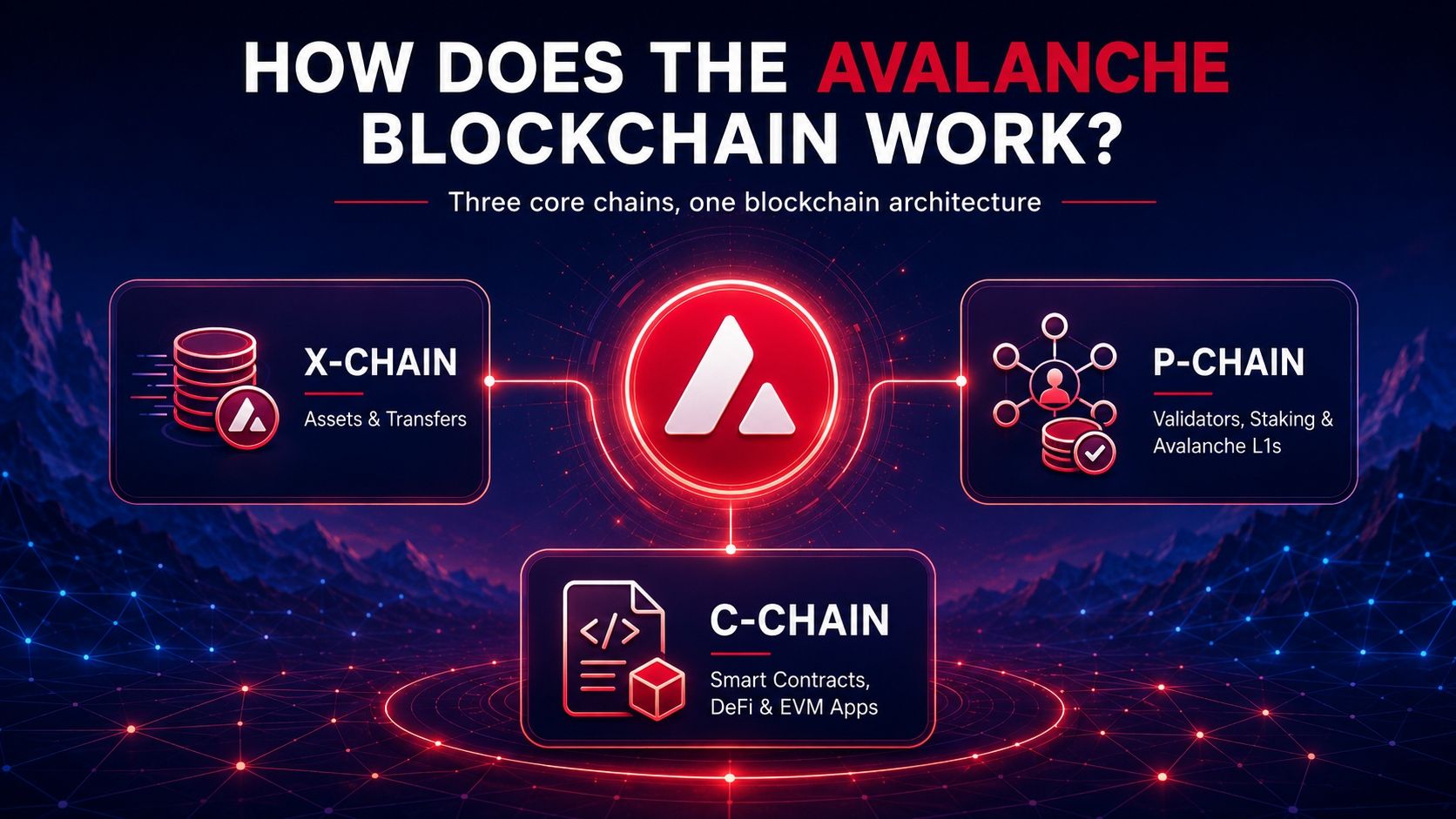

Avalanche: Another Blockchain Built for Tokenized Finance

Robinhood Chain is part of a broader movement toward blockchains designed for financial institutions, tokenized assets and specialized applications.

Avalanche has pursued a similar strategy through customizable networks, institutional blockchain deployments and infrastructure built for real-world assets. While the two ecosystems follow different models, both illustrate how blockchain technology is becoming increasingly tailored to specific financial use cases.

Learn more: What Is the Avalanche Blockchain and How Does It Work?

Disclaimer: This article is provided for informational purposes only and does not constitute investment, financial or legal advice. Cryptocurrencies, tokenized securities, DeFi products and Stock Tokens involve significant risks, including possible loss of capital, counterparty failure, limited liquidity, regulatory changes and technical vulnerabilities. Always conduct your own research and verify whether a product is legally available in your jurisdiction.