Only one week after its mainnet launch, Robinhood Chain volume surged to more than $560 million across decentralized exchanges in a single day. The sudden acceleration allowed Robinhood’s new blockchain to temporarily overtake Hyperliquid in reported 24-hour DEX spot volume.

For a network that officially went live on July 1, 2026, the milestone was remarkable.

The Robinhood Chain ecosystem did not need months or years to attract its first major wave of trading activity. Within days, the network had gained decentralized exchanges, lending markets, stablecoin liquidity, thousands of newly created tokens and a rapidly expanding community of speculative traders.

The event immediately raised an important question: what was really driving the Robinhood Chain volume?

Part of the answer came from Robinhood’s powerful brand, its existing user distribution and the arrival of major DeFi infrastructure. Uniswap supplied decentralized trading, Morpho attracted lending liquidity, Chainlink supported onchain data, and several stablecoins gave users assets with which to trade and provide collateral.

But another part of the answer was far more speculative.

Memecoins, new trading pairs and short-term opportunities played a major role in the initial boom. CASHCAT, the most visible token of the launch period, reportedly generated close to $98 million in daily volume on its own.

Robinhood Chain therefore experienced two launches at the same time: the launch of a serious financial infrastructure designed for tokenized assets, and the launch of a permissionless crypto market driven by the same speculative forces seen on Solana, Base and other fast-growing networks.

Even if daily figures later decline, the first week of the Robinhood Chain ecosystem will remain historically significant. It showed that a mainstream financial platform can launch a new blockchain and attract substantial liquidity almost immediately.

Robinhood Chain Volume Surpasses Hyperliquid

On July 8, 2026, decentralized exchanges operating on Robinhood Chain processed approximately $563.9 million in trading volume over 24 hours, according to market reports based on blockchain data.

Other snapshots placed the total between roughly $560 million and $570 million. The exact number varies because DEX statistics are continuously updated and different dashboards may apply slightly different classifications.

At that point, Robinhood Chain volume was higher than the comparable 24-hour DEX figure reported for Hyperliquid.

Another later comparison showed Robinhood Chain generating approximately $433 million in daily DEX trading, against about $296 million for Hyperliquid over the same observation period.

These figures did not mean that Robinhood Chain had permanently become a larger trading ecosystem than Hyperliquid. They showed that, during specific 24-hour periods, Robinhood Chain processed more decentralized spot trading activity.

That distinction matters.

Hyperliquid is particularly known for perpetual futures, its onchain order book and sophisticated derivatives trading. Robinhood Chain’s early surge was concentrated mainly in decentralized spot exchanges, WETH pairs and newly launched tokens.

Comparing the two networks therefore provides a useful indication of market attention, but not a complete comparison of their economic importance.

Nevertheless, the symbolic impact was considerable.

Hyperliquid had already established itself as one of the most important decentralized trading platforms in crypto. For a blockchain launched only one week earlier to temporarily exceed its reported daily DEX volume demonstrated how rapidly liquidity can now move between ecosystems.

Key takeaway: Robinhood Chain did not permanently replace Hyperliquid as a leading decentralized trading venue. But surpassing it in 24-hour DEX spot volume only days after launch was an exceptional milestone for a new blockchain.

A Historic Start for a New Blockchain

Most new blockchain networks face the same problem: they may have advanced technology, but they begin without users, liquidity or recognizable applications.

Creating a technically functional chain is no longer enough. A network also needs wallets, stablecoins, decentralized exchanges, oracles, bridges, lending markets and assets that people actually want to trade.

Robinhood Chain began with an advantage that most independent blockchain projects do not have: distribution.

Robinhood is already a widely recognized financial platform. It has experience serving retail investors across stocks, ETFs, options and cryptocurrencies. It also has a large audience that understands trading, even when many of those users are not familiar with advanced blockchain infrastructure.

This gave the company the ability to launch a network with immediate visibility.

The Robinhood Chain mainnet officially launched on July 1, 2026 as part of a broader international expansion involving Stock Tokens, DeFi products and agentic trading services.

The network was built using Arbitrum technology and remains compatible with the Ethereum ecosystem. Developers can therefore use familiar Ethereum tools while benefiting from a dedicated environment designed around Robinhood’s financial strategy.

Only one week after that launch, Robinhood Chain volume was already reaching several hundred million dollars across decentralized exchanges.

Whether those early volumes prove sustainable or not, the speed of the launch created an important historical precedent.

A major financial application had demonstrated that it could convert brand recognition, integrations and speculative attention into immediate onchain activity.

What Drove the Robinhood Chain Volume?

There was no single cause behind the record. The initial Robinhood Chain volume resulted from several forces appearing at the same time.

These included:

- The credibility and distribution associated with the Robinhood name;

- Low-cost and fast transactions;

- Uniswap liquidity and newly created trading pairs;

- Morpho lending markets and stablecoin deposits;

- The arrival of external wallets and infrastructure providers;

- Thousands of newly launched tokens;

- Speculative interest in Robinhood-themed memecoins;

- Expectations surrounding Stock Tokens and real-world assets;

- The search for early opportunities on a newly launched blockchain.

This combination is important because it separates the Robinhood Chain ecosystem from a closed financial database.

Robinhood could have built a private settlement layer used only for its own tokenized products. Instead, the network was presented as a public and permissionless blockchain on which external developers and traders could interact.

That openness allowed activity to develop beyond Robinhood’s official products.

It also exposed the network to the chaotic side of permissionless markets. Alongside institutional-sounding themes such as tokenized equities and onchain finance, Robinhood Chain immediately became a venue for memecoins and highly speculative tokens.

This may appear contradictory, but it is common in crypto.

The same infrastructure that supports stablecoins, lending and real-world assets can also allow anyone to issue and trade a new token within minutes.

Uniswap Became the Main Trading Engine

Uniswap played a central role in the initial expansion of the Robinhood Chain ecosystem.

A blockchain can attract many tokens, but those assets need a functioning market. Without decentralized exchanges and liquidity pools, users cannot easily buy or sell them.

Uniswap provided that trading layer.

Many of the most active markets involved WETH, stablecoins and newly issued tokens. Traders could move capital into liquidity pools, exchange assets and speculate on projects launched during the network’s first days.

This gave Robinhood Chain an immediate advantage over networks that launch without a major decentralized exchange.

Uniswap is familiar to Ethereum users and liquidity providers. Its presence reduced the amount of new infrastructure that participants had to learn.

Instead of relying entirely on an unfamiliar exchange created specifically for Robinhood Chain, users could interact with a protocol they already understood.

However, large DEX volume does not automatically imply deep or stable liquidity.

The same capital can be traded repeatedly during periods of intense speculation. A network with relatively modest liquidity can therefore generate very high turnover if traders frequently enter and exit positions.

For this reason, daily volume should always be analyzed alongside:

- Total value locked;

- Available liquidity in major pools;

- Trading depth and price impact;

- Unique active traders;

- Stablecoin supply;

- The concentration of volume among a small number of tokens.

The first Robinhood Chain volume record demonstrated strong activity. It did not, by itself, prove that the network already had the same market depth or maturity as older ecosystems.

CASHCAT Became the Symbol of the Launch

The token most closely associated with Robinhood Chain’s initial trading boom was CASHCAT.

CASHCAT was a memecoin traded primarily through Uniswap pairs on the new network. During the height of the first speculative wave, it reportedly generated close to $98 million in 24-hour trading volume.

Its market capitalization moved above $100 million during the initial surge, although estimates varied significantly as the price changed.

This was not a minor contribution.

If the reported figures are compared with Robinhood Chain’s approximately $563.9 million record, CASHCAT alone represented a substantial portion of total daily DEX activity.

The token therefore became both a symbol and a source of controversy.

Supporters saw the activity as evidence that Robinhood Chain could quickly attract traders, liquidity and community participation.

Critics argued that a memecoin-driven boom did not validate the network’s original purpose of supporting tokenized stocks, real-world assets and modern financial applications.

Both interpretations contain some truth.

CASHCAT did not prove that tokenized finance had already achieved mass adoption on Robinhood Chain. It did prove that the network was capable of generating a permissionless market with real demand and substantial turnover.

Memecoins often perform an unexpected role during the launch of a blockchain. They attract users, encourage wallet creation, generate transaction fees and motivate liquidity providers to move capital to a new ecosystem.

The danger is that this activity can disappear as quickly as it arrives.

A memecoin can rise dramatically, produce enormous volume and then lose most of its liquidity when traders move to the next opportunity.

The long-term success of the Robinhood Chain ecosystem will therefore depend on whether the infrastructure and capital attracted during the CASHCAT period remain active after the speculative excitement fades.

Thousands of Tokens Arrived on Robinhood Chain

The rapid increase in Robinhood Chain tokens was another sign of the network’s early momentum.

Reports indicated that approximately 16,000 tokens were created during one particularly active day, while several memecoins reached valuations above $1 million.

This does not mean that 16,000 established altcoin projects officially migrated to Robinhood Chain.

The distinction is important.

Permissionless token creation allows developers—or almost anyone with the necessary tools—to launch new assets quickly. Many of these tokens may have little liquidity, no long-term development plan and no practical utility.

The surge should therefore be described as an explosion in token creation, rather than an arrival of thousands of proven crypto projects.

Still, the figures reveal something meaningful about activity across the Robinhood Chain ecosystem.

Developers and traders clearly saw an opportunity in Robinhood Chain’s launch. Token creators moved rapidly to establish communities and capture attention before the ecosystem became more competitive.

The same pattern has occurred on other successful blockchains.

When a new network combines low fees, accessible tools and visible liquidity, token creation can accelerate dramatically. A small number of assets may survive and develop active communities, while the majority disappear.

For Robinhood Chain, the challenge is attracting more than short-lived launches.

A durable ecosystem needs:

- Recognized crypto assets with reliable liquidity;

- Stablecoins that can support trading and lending;

- DeFi protocols with sustainable revenue;

- Tokenized real-world assets with clear legal structures;

- Developers building products beyond memecoin speculation.

Morpho and the Growth of Lending Liquidity

While memecoins generated much of the attention, Morpho represented the more structural side of the Robinhood Chain launch.

Morpho provides decentralized lending markets in which users can supply assets, earn yield or borrow against collateral.

The protocol was selected to support Robinhood Earn, an onchain product designed to connect users with lending opportunities.

During the launch period, Morpho attracted a large share of the network’s deposited liquidity. Reports indicated that tens of millions of dollars were placed in lending markets involving stablecoin assets.

This is important because lending deposits behave differently from rapid DEX trading.

A trader can generate significant volume by repeatedly exchanging the same funds. Lending liquidity usually represents capital deposited into a protocol and made available to borrowers.

Morpho therefore offered another way to evaluate the Robinhood Chain ecosystem.

If lending deposits remain stable, borrowing demand develops and suppliers continue earning competitive yields, this activity could provide a more durable foundation than temporary memecoin turnover.

However, lending growth also introduces additional risks.

Users must consider:

- Smart-contract vulnerabilities;

- Oracle accuracy;

- Collateral quality;

- Stablecoin depegging;

- Liquidation risk;

- Concentration in a small number of depositors;

- Whether yields are organic or subsidized.

High deposits at launch can be supported by promotional incentives. The real test is whether liquidity remains after introductory rewards or unusually attractive yields decline.

Stablecoins Provided the Liquidity Base

Stablecoins are essential to almost every active DeFi ecosystem.

They provide a relatively stable unit of account for traders, collateral for lending protocols and a method of moving dollar-denominated liquidity between applications.

The Robinhood Chain ecosystem quickly attracted substantial stablecoin value during its first days.

The presence of assets connected to established stablecoin and DeFi ecosystems allowed traders to enter markets without relying entirely on volatile cryptocurrencies.

Stablecoins also supported the two main sources of early activity:

- DEX trading through pairs involving stable assets or WETH;

- Lending deposits through protocols such as Morpho.

The growth of stablecoin supply is therefore one of the most important indicators to follow after the initial Robinhood Chain volume record.

If stablecoin liquidity remains on the network, it can support future applications even after speculative token turnover declines.

If stablecoin balances fall rapidly, it may indicate that capital entered mainly to capture temporary incentives or short-term trading opportunities.

The quality of stablecoin liquidity also matters.

A network dependent on a single stablecoin, bridge or small group of large holders may appear liquid while remaining vulnerable to sudden withdrawals.

A healthier ecosystem would gradually develop diversified liquidity across several widely used assets and multiple applications.

Was the Robinhood Chain Volume Organic?

The word “organic” is difficult to define in crypto markets.

Almost every new blockchain uses some combination of incentives, partnerships, marketing and early-user rewards to attract capital.

The surge in Robinhood Chain volume was real in the sense that actual onchain trades occurred. Users created wallets, exchanged tokens and supplied liquidity.

But that does not mean all of the activity represented long-term demand.

Several factors may have amplified the initial figures:

- Launch-related incentives;

- Low or subsidized transaction costs;

- Memecoin speculation;

- Repeated trading by the same users;

- Automated bots;

- Possible expectations of future rewards;

- Traders attempting to establish an early position in the ecosystem.

The unusually high relationship between trading volume and available liquidity suggests that some capital may have changed hands many times during the same period.

This is not necessarily fraudulent or artificial. High turnover is normal when a new token becomes extremely volatile.

However, it means the headline volume should not be interpreted as hundreds of millions of dollars in entirely new capital entering Robinhood Chain each day.

Volume measures the total value of trades. It does not measure net inflows.

A trader buying $10,000 of a token and later selling the same position generates approximately $20,000 of gross trading volume, even though only $10,000 was initially deployed.

The distinction is essential when evaluating the record.

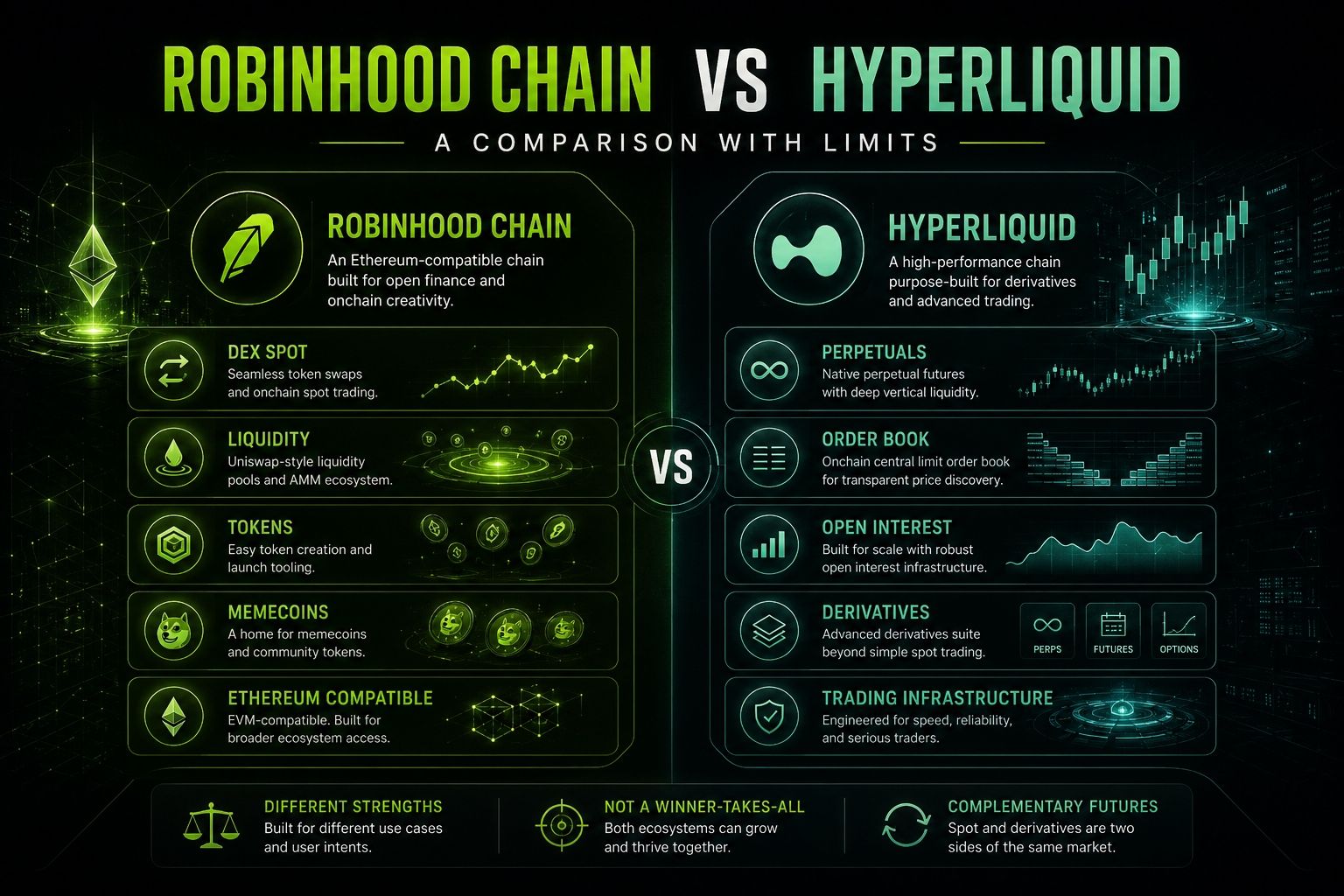

Robinhood Chain vs Hyperliquid: A Comparison With Limits

The headline comparison with Hyperliquid attracted attention because Hyperliquid is one of the strongest names in decentralized trading.

However, Robinhood Chain vs Hyperliquid is not a perfectly equivalent comparison.

Robinhood Chain is an Ethereum-compatible blockchain supporting multiple applications, including decentralized exchanges, lending markets, token creation and potentially tokenized securities.

Hyperliquid operates a highly specialized trading ecosystem recognized primarily for perpetual futures and onchain order-book execution.

The reported comparison focused on a specific category: 24-hour decentralized exchange volume.

It did not mean Robinhood Chain had surpassed Hyperliquid in:

- Perpetual futures volume;

- Open interest;

- Protocol revenue;

- Trading depth;

- Long-term user retention;

- Cumulative trading activity;

- Market influence.

Robinhood Chain’s DEX activity was also distributed through applications such as Uniswap, while Hyperliquid’s liquidity is closely associated with its own trading infrastructure.

The most accurate conclusion is therefore narrower but still impressive:

Robinhood Chain temporarily generated more reported daily decentralized spot trading volume than Hyperliquid only one week after its mainnet launch.

That remains an important milestone without requiring an exaggerated interpretation.

Why Robinhood’s Brand Changed the Launch Dynamic

Blockchain networks traditionally build distribution after launch.

Robinhood approached the problem from the opposite direction. It had distribution before the network existed.

The company already possessed:

- A recognizable global financial brand;

- An established retail trading application;

- Experience with stocks, ETFs and cryptocurrencies;

- Relationships with market makers and infrastructure providers;

- The ability to promote new products to an existing audience.

This made Robinhood Chain fundamentally different from an anonymous Layer 1 or Layer 2 project launching with only a technical white paper and a token incentive program.

Robinhood did not need to convince the market that it could attract financial users in theory. It already had them.

The larger challenge is moving those users onchain.

Many Robinhood customers may not want to manage private keys, bridges, gas fees or decentralized applications. The company must therefore make the blockchain experience simple enough that users can benefit from onchain infrastructure without confronting all of its complexity.

The first Robinhood Chain volume record came mainly from crypto-native activity. The next stage will involve connecting that activity with Robinhood’s broader financial audience.

Tokenized Stocks Were Not the Main Driver of the Record

Robinhood Chain was introduced as infrastructure for Stock Tokens, tokenized ETFs, real-world assets and DeFi.

It would therefore be easy to assume that the record volume was primarily generated by tokenized equities.

That was not the case.

The largest early trading flows were associated with WETH pairs, memecoins and crypto-native assets.

This does not invalidate Robinhood’s tokenization strategy. It shows that permissionless crypto markets can develop faster than regulated financial products.

Launching a memecoin requires limited legal infrastructure. Launching a token representing an equity requires custody, disclosures, compliance rules, geographic restrictions and a clear legal relationship with the underlying asset.

Tokenized stocks are therefore likely to develop more slowly.

The early crypto activity may still benefit Robinhood’s longer-term strategy by creating:

- Active wallets;

- Liquidity providers;

- DEX infrastructure;

- Stablecoin balances;

- Developer familiarity;

- Oracle and bridge integrations.

These components could later support tokenized financial assets.

The critical question is whether Robinhood can connect the permissionless crypto ecosystem with regulated Stock Tokens without creating confusion about what users actually own.

What the Record Means for the Robinhood Chain Ecosystem

The record proved several things about the Robinhood Chain ecosystem.

First, the network can attract attention.

Thousands of tokens, rapidly increasing wallet activity and hundreds of millions of dollars in trading turnover demonstrated strong awareness among crypto users.

Second, Robinhood can coordinate important integrations.

Uniswap, Morpho and infrastructure providers gave the network useful applications from the beginning.

Third, traders are willing to move between chains quickly.

Blockchain loyalty is often weaker than it appears. Users follow liquidity, narratives, incentives and opportunities. Robinhood Chain became an attractive destination because it combined all four.

Fourth, a mainstream brand can accelerate blockchain adoption.

Robinhood’s identity gave the network visibility that would have taken an unknown project much longer to achieve.

Finally, speculative demand remains one of the fastest ways to activate a blockchain.

Robinhood Chain was designed around serious themes such as tokenized finance, yet its first historic volume record was strongly connected to a cat-themed memecoin.

This contrast says as much about the crypto market as it does about Robinhood.

Could Robinhood Chain Challenge Base and Solana?

The initial volume surge naturally led to comparisons with Base and Solana.

Base has demonstrated how a major American crypto platform can use distribution to build a broad onchain ecosystem. Coinbase provides the brand and user access, while developers create applications, social products, trading venues and tokens.

Robinhood appears to be pursuing a related model, but with a stronger emphasis on brokerage products and tokenized financial assets.

Solana represents another relevant comparison. Its low fees and fast transactions have made it one of the leading networks for decentralized trading and memecoin activity.

Robinhood Chain’s first week resembled parts of the Solana experience: rapid token creation, speculative communities and high-volume DEX trading.

However, one successful week does not establish Robinhood Chain as a direct rival to either network.

Base and Solana have:

- Much larger established developer communities;

- Broader application ecosystems;

- Longer operating histories;

- More diversified liquidity;

- Greater evidence of user retention.

The Robinhood Chain ecosystem has shown that it can attract an initial wave. It must now prove that it can retain users and support applications after the launch narrative becomes less powerful.

The Indicators That Matter After the Launch

Daily Robinhood Chain volume will continue attracting headlines, but several other indicators will provide a better picture of long-term development.

Stablecoin supply

Stablecoins remaining on the network can support trading, lending and real-world assets. Persistent growth would indicate that capital is staying rather than immediately leaving.

Total value locked

TVL provides an estimate of assets deposited in DeFi protocols. It should be analyzed carefully because incentive-driven deposits can disappear rapidly.

Active users

A large number of unique wallets is positive, but retention matters more. The key question is how many users remain active several weeks or months later.

Trading concentration

A healthy ecosystem should not depend entirely on one memecoin or one liquidity pool. Volume distributed across several credible assets would be more sustainable.

Lending demand

Morpho deposits become more meaningful if they support actual borrowing and economic activity rather than sitting in subsidized pools.

Protocol revenue

Applications generating fees without excessive token incentives are more likely to survive.

Real-world asset adoption

Robinhood Chain’s original strategy centers on Stock Tokens and tokenized finance. The growth of legally structured RWAs may ultimately matter more than memecoin turnover.

Developer activity

A durable blockchain requires teams building products over months and years, not only launching tokens during the first week.

The Main Risks Behind the Volume Boom

The spectacular launch also introduced significant risks.

Memecoin concentration

When a large share of volume depends on one speculative token, activity can fall sharply if interest disappears.

Liquidity reversals

Capital can move into a new chain rapidly, but it can leave just as quickly. Bridges and stablecoin outflows should be monitored.

Wash trading and automated activity

High turnover may include bots or strategies designed to generate activity. Volume alone does not reveal the quality of demand.

Smart-contract risk

New applications may not have been tested under all market conditions. Bugs, oracle failures and liquidity-pool exploits can cause losses.

Token-launch scams

Permissionless creation allows legitimate experimentation, but it also makes it easier to launch fraudulent tokens, copy recognizable brands or remove liquidity from buyers.

Regulatory uncertainty

Robinhood’s broader vision involves tokenized securities. The legal treatment of these products remains complex, particularly in the United States.

Brand confusion

Users may incorrectly assume that every asset launched on Robinhood Chain is issued or approved by Robinhood. A public blockchain can host unofficial projects with no direct relationship to the company.

Important: A token operating on Robinhood Chain is not automatically a Robinhood product. Users should verify the issuer, contract address, liquidity and legal structure before interacting with any asset.

Why This Event Will Remain Historically Important

Crypto trading volumes change every day. The ranking that placed Robinhood Chain above Hyperliquid was temporary.

The event remains important because of how quickly it occurred.

The Robinhood Chain volume milestone proved that a new blockchain backed by a major financial platform could move from launch to hundreds of millions of dollars in daily trading activity in approximately one week.

That speed would have seemed extraordinary during earlier blockchain cycles, when networks often needed months to obtain bridges, stablecoins and usable decentralized exchanges.

The launch of the Robinhood Chain ecosystem reflected a more mature and interconnected crypto market.

Infrastructure can now be deployed rapidly. Liquidity can cross networks through bridges. Ethereum-compatible applications can expand to new chains with less development work. Traders can move as soon as an opportunity appears.

The result is a blockchain market in which adoption can accelerate almost instantly.

This also creates a new competitive environment.

Coinbase, Robinhood, financial technology companies and traditional institutions may increasingly launch or support their own onchain infrastructure. Their greatest advantage will not necessarily be superior blockchain technology.

It will be distribution.

The platforms able to connect existing customers with blockchain applications may activate new ecosystems much faster than purely crypto-native projects.

Can Robinhood Chain Turn an Explosive Launch Into Lasting Success?

The initial Robinhood Chain volume established awareness. It did not guarantee long-term success.

The network’s next phase will depend on whether it can move beyond three temporary forces:

- Launch incentives;

- Memecoin speculation;

- The novelty of a Robinhood-branded blockchain.

For Robinhood Chain to become a durable financial network, it will need more persistent sources of demand.

These could include:

- Tokenized stocks and ETFs with clear investor rights;

- Real-world assets generating sustainable yield;

- Stablecoin payments and settlement;

- Active lending and borrowing markets;

- Decentralized exchanges with deep liquidity;

- Applications serving Robinhood’s international user base;

- Tools that make blockchain complexity invisible to retail customers.

Robinhood does not need to maintain a record volume every day for the launch to be considered successful.

It needs to convert part of the temporary activity into lasting infrastructure, capital and user behavior.

Even a significant decline from the first-week peak would not erase what the launch demonstrated.

The historical fact would remain: the Robinhood Chain ecosystem became one of the most actively traded new blockchain networks almost immediately.

Conclusion: Robinhood Chain Established a New Launch Model

The surge in Robinhood Chain volume was one of the most striking blockchain launches of 2026.

Only one week after the network went live, its decentralized exchanges processed approximately $563.9 million in daily volume and temporarily surpassed Hyperliquid in a comparable 24-hour DEX ranking.

The achievement was powered by several forces.

Robinhood brought brand recognition and distribution. Uniswap provided decentralized trading. Morpho attracted lending liquidity. Stablecoins gave traders a financial base. Thousands of tokens arrived, while CASHCAT became the speculative symbol of the network’s first week.

The record should not be misunderstood.

It did not mean Robinhood Chain had permanently overtaken Hyperliquid or become more important than established ecosystems such as Ethereum, Solana or Base.

It also did not show that tokenized stocks were already responsible for most network activity.

Much of the first boom came from memecoins, WETH pairs and speculative trading.

But those nuances do not eliminate the historical significance of the event.

The Robinhood Chain volume surge demonstrated that a mainstream financial company can launch a public blockchain and generate substantial onchain activity almost immediately.

Even if the record is never repeated, the launch has already established a precedent.

The next question is no longer whether Robinhood can attract attention to its blockchain. It has already done that.

The question is whether Robinhood Chain can transform a spectacular first week into a lasting ecosystem for DeFi, tokenized securities and global onchain finance.

Robinhood Chain Volume FAQ

How much DEX volume did Robinhood Chain record?

Robinhood Chain volume reportedly reached approximately $563.9 million across decentralized exchanges on July 8, 2026. Other market snapshots placed the figure between roughly $560 million and $570 million, depending on the observation time and data provider.

Did Robinhood Chain really surpass Hyperliquid?

Yes. During specific 24-hour observation periods, Robinhood Chain volume exceeded the reported DEX spot volume generated by Hyperliquid. However, this did not mean that the Robinhood Chain ecosystem had permanently become larger than Hyperliquid across derivatives trading, open interest, liquidity or cumulative activity.

When did Robinhood Chain launch?

The Robinhood Chain mainnet officially launched on July 1, 2026. Its first major Robinhood Chain volume record was reported approximately one week later, making the speed of the network’s early growth especially notable.

What caused the Robinhood Chain volume surge?

The initial Robinhood Chain volume surge was driven by Uniswap trading, WETH pairs, stablecoin liquidity, Morpho deposits, low transaction costs, thousands of newly created tokens and intense memecoin speculation.

What role did CASHCAT play in Robinhood Chain volume?

CASHCAT became the most visible memecoin in the early Robinhood Chain ecosystem. It reportedly generated close to $98 million in 24-hour volume during the peak period, making it a significant contributor to the overall Robinhood Chain volume record.

Were tokenized stocks responsible for the Robinhood Chain volume record?

Not primarily. Most early Robinhood Chain volume came from crypto-native assets, WETH pairs, newly launched tokens and memecoins rather than Stock Tokens or tokenized equities.

How many tokens launched in the Robinhood Chain ecosystem?

Reports indicated that approximately 16,000 tokens were created during one particularly active day. This reflected rapid expansion across the Robinhood Chain ecosystem, but it did not mean that thousands of established altcoin projects had officially migrated to the network.

Is Robinhood Chain volume sustainable?

It is still too early to know whether Robinhood Chain volume can remain close to its launch-period highs. Sustainable growth will depend on user retention, stablecoin liquidity, protocol revenue, lending activity, developer participation and the adoption of tokenized real-world assets.

Is Robinhood Chain bigger than Hyperliquid?

Not based on one daily volume comparison. Hyperliquid has an established derivatives ecosystem, substantial open interest and a longer operating history. The Robinhood Chain ecosystem only exceeded it in a specific daily DEX spot volume metric during the launch period.

What are the main risks for the Robinhood Chain ecosystem?

The main risks facing the Robinhood Chain ecosystem include speculative token concentration, sudden liquidity outflows, smart-contract vulnerabilities, unofficial or fraudulent tokens, regulatory uncertainty and excessive dependence on launch incentives.

Why was Robinhood Chain’s launch historically important?

The launch showed that a mainstream financial platform can use its brand, distribution and partnerships to create a highly active Robinhood Chain ecosystem within days. Even if Robinhood Chain volume later declines, the speed of the initial expansion remains an important historical milestone for blockchain adoption.

What could support future Robinhood Chain volume growth?

Future Robinhood Chain volume could be supported by deeper Uniswap liquidity, continued Morpho activity, more stablecoin deposits, recognized crypto assets, Stock Tokens, real-world assets and new applications joining the Robinhood Chain ecosystem.

What should investors monitor in the Robinhood Chain ecosystem?

The most important indicators include Robinhood Chain volume, stablecoin supply, total value locked, active wallets, protocol revenue, lending demand, trading concentration and the number of credible developers building within the Robinhood Chain ecosystem.

What Is Robinhood Chain and How Does It Work?

The record trading volume is only one part of Robinhood’s broader blockchain strategy. Robinhood Chain was designed to support Stock Tokens, real-world assets, decentralized exchanges, lending and programmable financial services.

Discover how its technology works, why Robinhood built its own blockchain and which regulatory and DeFi risks investors should understand.

Read the complete guide: What Is Robinhood Chain? Tokenized Stocks, DeFi and Key Risks.

Disclaimer: This article is provided for informational purposes only and does not constitute investment or financial advice. Blockchain networks, decentralized finance applications, memecoins and tokenized assets involve significant risks, including volatility, loss of capital, smart-contract failures, liquidity problems and regulatory changes. Always conduct your own research before using a blockchain application or purchasing a digital asset.